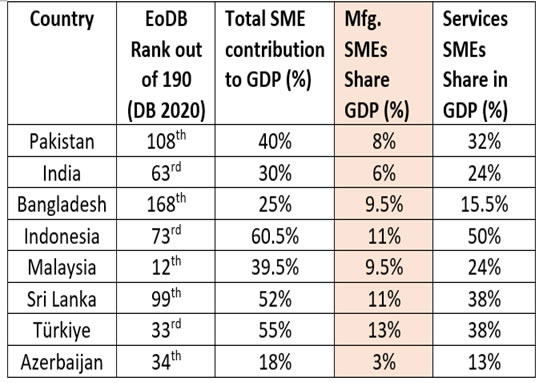

Ease of Doing Business (EoDB) refers to the administrative, legal, and institutional conditions, shaping how efficiently firms can start and operate. Globally, high EoDB economies record over 55% GDP contribution from Small and Medium Enterprises) SMEs, indicating a strong association between regulatory efficiency and SME-driven economic activity. In Pakistan SMEs contribute around 40% of the GDP, with 32% from services sector and just 8% from 696,000 manufacturing units. Although Pakistan’s EoDB ranking improved from 144th in 2017 to 108th in 2020, but the manufacturing SME’s share remained stagnant (Table 1).

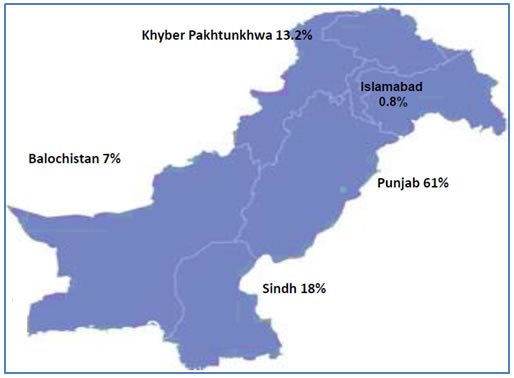

Figure 1: Geographical Dispersion of SMEs in Pakistan

Sources: SMEDA (exact data on GB and AJ&K SMEs is not available)

Therefore, this insight dissects the regulatory and practical bottlenecks in EoDB in Pakistan through the lens of manufacturing SMEs. Pakistan’s SME framework is defined by the National SME policy (2021), which classifies firms with an annual turnover of Rs 150-800 million as SME. Currently, around 5.2 million SMEs operate in the country.

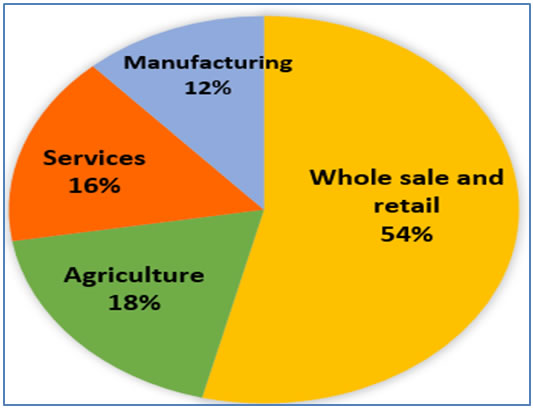

They make up 90% of all enterprises, while large-scale manufacturers account for only 10%. The geographical dispersion and sectoral classification of SMEs are shown in fig 1 & 2, respectively. Within this ecosystem, just 12% SMEs belong to manufacturing sector, thus making it the smallest sector, contributing 30% to the total exports.

Figure 2: Sectoral Classification of SMEs in Pakistan

Sources: SMEDA

A cross-country comparison of Ease of Doing Business and SME contribution reveals that countries with relatively favourable business environments not only record higher overall SME contribution to GDP, but also demonstrate stronger manufacturing SME participation (Table 1).

Malaysia (10%), Türkiye (13%), and India (6%) reflect varying degrees of manufacturing SME integration into broader industrial and global value chains. This suggests that a supportive business environment plays a critical role in enabling SMEs to scale and integrate into international manufacturing networks.

Table 1: Cross-country comparison of SME contribution to GDP

Sources: Compiled by Author from World Bank Doing Business Report

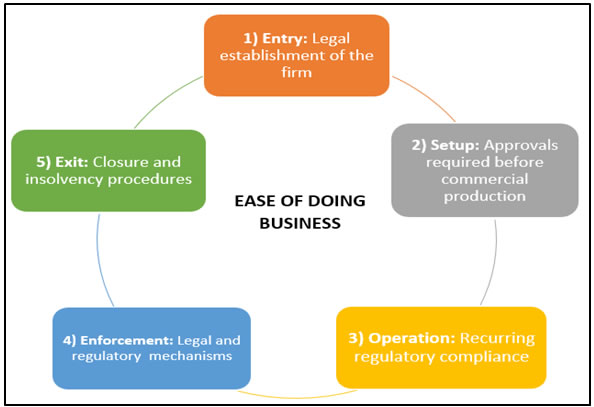

To contextualise the EoDB landscape for SMEs, this analysis uses a life-cycle framework that maps the firm’s regulatory journey across 5 stages: entry, setup, operation, enforcement, and exit (figure 3), adopting a Composite Indicative Index (CII) scoring approach, whose details are as follows;

Figure 3: Life Cycle of an SME Firm

Sources: Created by Author

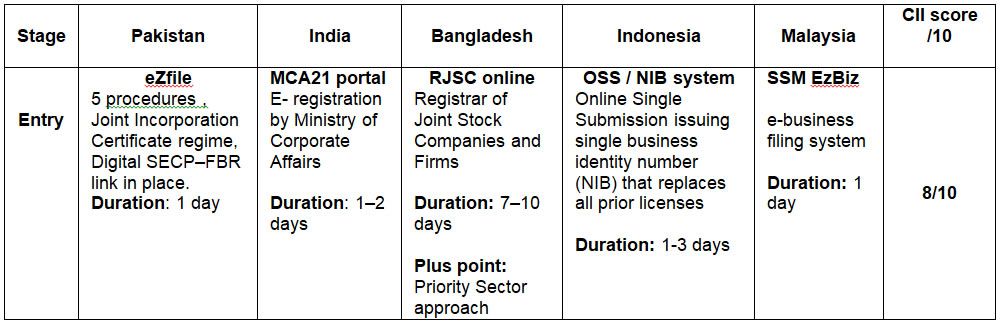

Firstly, ‘Entry’ refers to the cost, time, and procedures required to legally establish a firm. Pakistan ranks 6th among eight South Asian (SA) economies at this stage. Business registration previously was completed in 16-17 days through the Securities and Exchange Commission of Pakistan (SECP) and the Federal Board of Revenue (FBR). However, the eZfile reform of 2021 is enabling one-day registration through data-sharing among seven government agencies, resulting in a 51% increase in business registrations.

A comparative analysis of developing countries' EoDB indicates that these practices must be viewed beyond speed alone. For instance, Bangladesh complements streamlined registration with targeted filing and facilitation support for priority sectors, offering a useful model for strengthening manufacturing-oriented growth in Pakistan. Therefore, Pakistan’s entry-stage CII score is 8 out of 10, indicating a business-friendly environment.

Table 2: Comparative analysis of Entry Stage EoDB in Developing Countries

Sources: Compiled from official websites

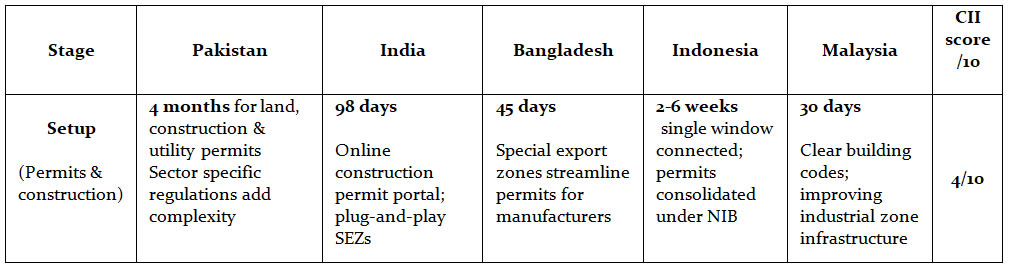

The second stage is ‘Setup’, covering permits, utility connections, and operational clearances required before manufacturing begins. Pakistan ranks 166th globally on this indicator. Previously, setup took 8-9 months due to fragmented zoning laws and multi-agency approvals. The Reforms strategy of 2020 by the Board of Investment reduced these procedural delays by 54% (approx. 4 months) by curbing manual registrations. However, high land transfer taxes and disjoint environmental, labour and hazard clearances continue to burden the firms. Best practices from comparable economies highlight integrated single-window systems and risk-based permit approvals as effective models for streamlining setup regulations. Against this backdrop, Pakistan’s setup stage CII score is 4 out of 10, reflecting a partially reformed but structurally constrained environment.

Table 3: Comparative analysis of Setup Stage EoDB in Developing Countries

Sources: Compiled by Author

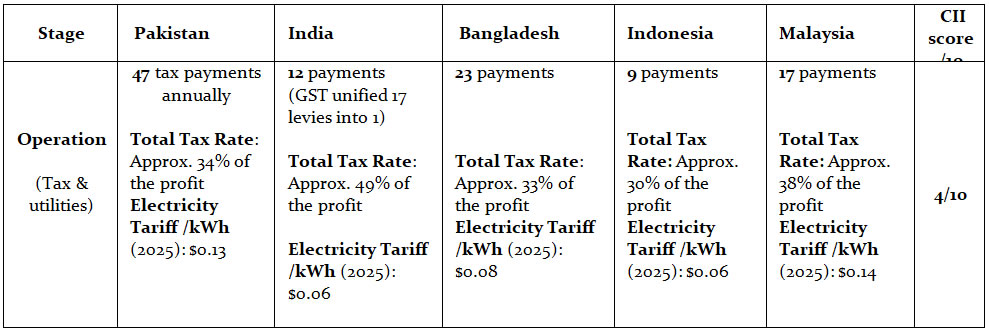

Third, ‘Operation’ stage involves running the enterprise, covering taxation and utilities. In terms of taxation regime, Pakistan ranks 173rd out of 190 economies and 7/8 regional economies. There are overlapping taxation layers from federal and provincial authorities requiring 47 payments as tax obligations, and incurring a total of 34% of commercial profit. In addition, access to manufacturing utilities is also low. According to Enterprise Survey data, 70% firms cite energy as the main constraint, with tariffs of 13.5 cents/ kWh making electricity the most expensive in the region. Additionally, frequent outages force reliance on backup power, causing losses of nearly 35% annually.

Best practices from comparable developing economies presents fewer tax payments as a reform that not only reduces administrative burden but also curtails avenues of rent-seeking and exploitation (Table 4). Against this backdrop, Pakistan’s ‘operation’ stage CII score is 4 out of 10, where administrative and policy interventions are crucial to enhance EoDB.

Table 4: Comparative analysis of Operation Stage EoDB in Developing Countries

Sources: Compiled by Author

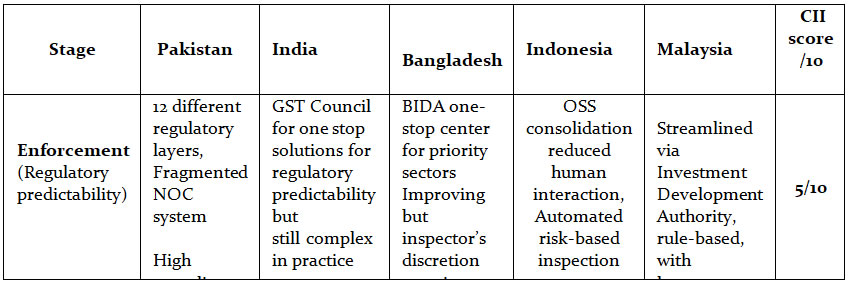

Fourth stage is ‘Enforcement’, involving regulatory predictability based on consistently applied regulations. Currently, at least 12 different regulatory layers with over 50 laws, enforced by 800 major regulators and thousands of processes and permits in the country. This bureaucratic complexity disproportionately affects small firms, which face nearly 70% higher operational burdens than large firms, according to Enterprise Survey Data.

Although initiatives such as Pakistan Single Window (PSW) and the Asaan Karobar aim to simplify procedures, limited awareness, constrain their effectiveness for many businesses. Best practices from developing and top EoDB countries present that employing an automated management system, reducing delays, uncertainty in regulatory mechanisms as a reform pathway. Against this benchmark, EoDB score of Pakistan is 5 out of 10.

Table 5: Comparative analysis of Enforcement Stage EoDB in Developing Countries

Sources: Compiled by Author

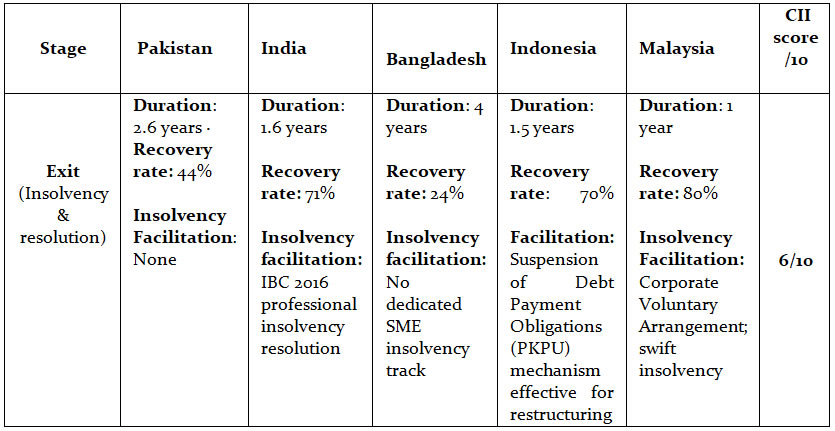

Final stage of EoDB journey is ‘Exit’, covering insolvency procedures that help rehabilitate viable businesses and efficiently liquidate non-viable ones, supporting healthy credit environment.

Insolvency procedures are assessed through recovery rate, resolution time, and cost under the legal framework. Pakistan’s insolvency cost stands at 4% of estate value, below the regional average of 10%, indicating a relatively easier exit environment. However, cases still take 2-3 years to resolve, with a recovery rate of only 44%.

Moreover, the Corporate Rehabilitation Act 2018 limits restructuring to firms with debts below PKR 100 million, excluding many SMEs and leaving liquidation as the main option. Best practices show that professionally facilitated insolvency systems can reduce resolution time to under 4 months and raise recovery rates to nearly 93%. Against this benchmark, Pakistan’s exit-stage EoDB score can be assessed at 6 out of 10.

Table 6: Comparative analysis of Exit Stage EoDB in Developing Countries

Sources: Compiled by Author

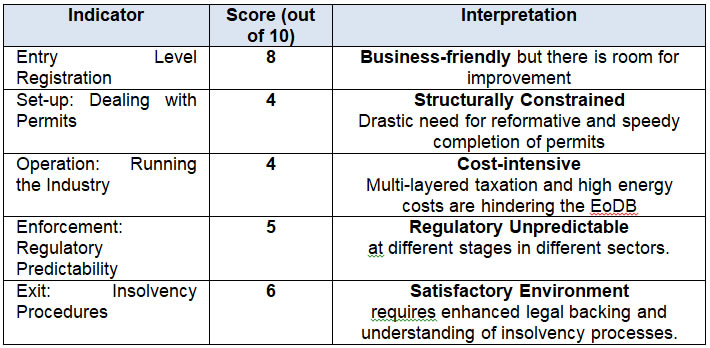

To conclude, Pakistan records an average EoDB score of 5.4/10, implying a structurally constrained environment, where operations and setup stage present to be the weakest link. In this regard, regional comparisons highlight that adopting single-window systems and ensuring regulatory predictability are important, but given the above analysis, there is a lack of a clear information facilitation mechanism, which is hindering EoDB at all stages, from entry till exit.

Table 7: Scorecard of EoDB in Pakistan

Sources: Compiled by Author

Scale Explanation

- 2-4 Restrictive Environment

- 4-6 Structurally Constrained

- 6-8 Moderate

- 8-10 Business Friendly

Although the government has undertaken reform initiatives like eZfile and the Leading Efficiency through Automation Prowess project (LEAP) aimed at enhancing digitisation, their limited understanding keeps businesses trapped in procedural delays. Therefore, ensuring that reforms are effectively communicated and implemented on the ground are critical to translating policy gains into actual business facilitation.